Navigating Your Connecticut Home Purchase with Confidence.

Choosing a home is about your family’s future. As your Neighborly Guardians, we bring sophisticated legal protection to your closing table, ensuring every detail of your purchase is handled with technical precision and care.

Reviewing the Real Estate Binder & Purchase Agreement.

In Connecticut, the "Binder" is the first legally binding step of your home purchase. As your counsel, we don't just oversee the paperwork; we actively negotiate mortgage contingency dates and inspection repair credits. We ensure your deposit is protected by airtight language, addressing liabilities like radon, oil tanks, or structural defects before you commit your capital.

Securing Your Marketable Title & Underwriting.

We perform an exhaustive 40-year back-search on land records to verify an unbroken chain of title. By resolving "clouds" such as unreleased mortgages or municipal liens, we secure your ownership. As authorized title underwriters, we issue Owner’s Insurance to defend your equity against hidden risks like fraud or clerical errors.

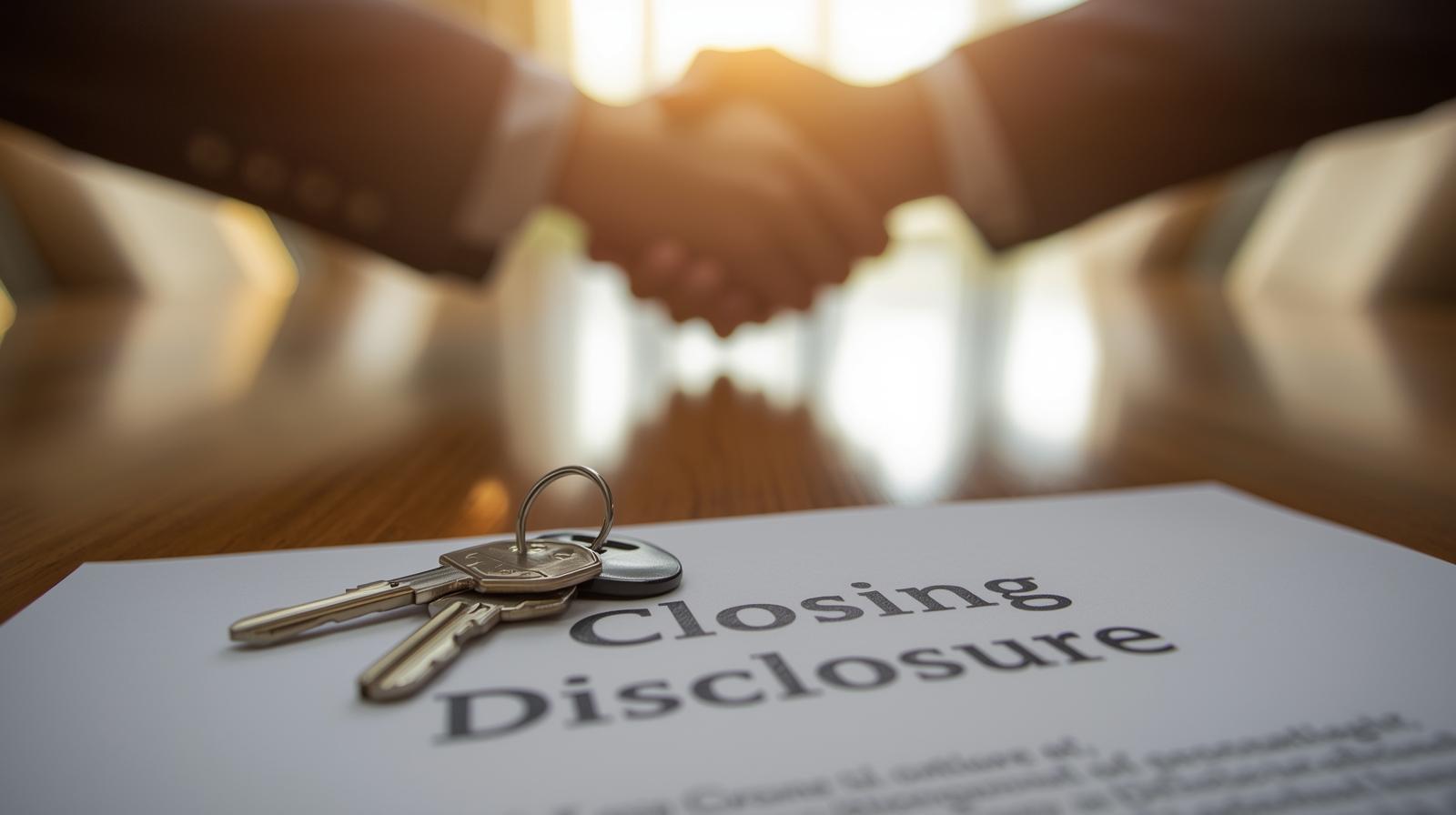

The Closing Disclosure & Municipal Adjustments.

The final 72 hours are about precision. We coordinate with your lender to finalize the Closing Disclosure (CD), verifying your interest rate and cash-to-close figures. We calculate municipal adjustments for property taxes and fuel oil prorations so that your final settlement is accurate, transparent, and free of last-minute surprises.

Frequently Asked Closing Questions.

Why is an attorney required in CT?

CT is an "Attorney State." A lawyer is legally required to conduct the title search, coordinate the mortgage funding, and record the warranty deed to officially transfer ownership.

What are Closing Adjustments?

These are prorated costs (taxes, water, sewer, fuel oil) that the seller has prepaid. We calculate exactly what you owe based on your specific closing date.

What is a Resale Certificate?

Essential for Condo buyers, this certificate reveals the HOA's financial health, pending lawsuits, and reserve funds to ensure you aren't buying into debt.

Who pays for Title Insurance?

The buyer pays for the lender's policy (required) and the owner's policy (optional but critical) to protect their own financial investment.